Mortgage Loans | Allowable Paid Closing Costs

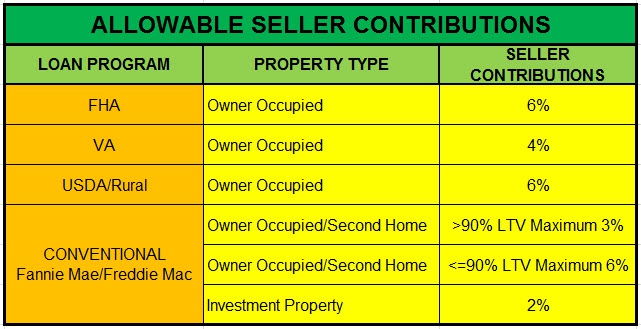

Most Mortgage Loans that I, George Soutu, do these days have Seller Paid Closing Costs. As a result of this, a common question I am asked often by Borrowers and Agents,is how much can they ask the Seller to contribute towards the Borrower’s Closing Costs? Given that I am asked this question often, I thought it would be useful to provide a chart with the Allowable Seller Paid Closing Cost for the four Loan Programs most Borrowers are doing these days. In the chart below are the Allowed Seller Paid Closing Costs For FHA, VA, USDA, & Conventional Loans:

Allowable Seller Closing Costs

FHA does have a restriction on allowable Seller Paid Closing Costs.

Sellers are not allowed to reimburse Borrowers for any Closing Costs paid before the Closing. For Example, many Lenders will collect the Appraisal Fee and Application Fee at the time of application. The Borrower cannot be reimbursed for these fees later at the Closing by the Seller. Also, if Homeowners Insurance is paid by the Borrower before the Closing, this cost also might not be able to be reimbursed by the Seller later at the Closing.

These are just a couple of examples, but this FHA guideline applies to all fees or expenditures paid by the Borrower before the Closing. However, a Borrower can be reimbursed for fees and expenses paid before the Closing if the Borrower is also applying for a Down payment and Closing Cost Assistance Loan (DAP). In this case FHA will allow the Borrower to role fees paid outside the Closing into the DAP Loan, and be reimbursed the funds at the Closing. Hope the chart helps to quickly and easily identify the Allowed Seller Paid Closing Costs For FHA, VA, USDA, & Conventional Loans, and provides a quick reference for future use when obtaining a mortgage. Mortgage Loans | Allowable Paid Closing Costs.

******************************************************************************

Info about the guest author: George Souto NMLS# 65149 is a Mortgage Loan Originator who can assist you with all your FHA,  CHFA, and Conventional #mortgage needs in Connecticut. George resides in Middlesex County Connecticut. George can be contacted at (860) 573-1308 or gsouto@mccuemortgage.com. I am pleased to have George be a guest contributor to my web site with his wealth of mortgage knowledge. He is an expert on mortgages and lending practices and is a great resource for all real estate agents.

CHFA, and Conventional #mortgage needs in Connecticut. George resides in Middlesex County Connecticut. George can be contacted at (860) 573-1308 or gsouto@mccuemortgage.com. I am pleased to have George be a guest contributor to my web site with his wealth of mortgage knowledge. He is an expert on mortgages and lending practices and is a great resource for all real estate agents.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~